“Practical men who believe themselves to be quite exempt from any intellectual influence, are usually the slaves of some defunct economist. Madmen in authority, who hear voices in the air, are distilling their frenzy from some academic scribbler of a few years back”

For those new to this blog, mediamacro is a term I coined for how macroeconomics is generally talked about in the media, particularly when discussing the general direction of fiscal policy. By implication it is very different to what economics students are taught. What I mean by mediamacro will become clear in this discussion.

The famous quote from Keynes is relevant, because with mediamacro the practical men were the vast majority of journalists who were convinced after the Global Financial Crisis (GFC) that governments had to tighten their belt, and the madmen were of course the politicians who made this their policy. But mediamacro survived the demise of the Cameron government, and continues to dominate the way many political journalists talk about the budget and other fiscal issues. A big reason for this is that many politicians, in all parties, still think keeping government debt to GDP falling is synonymous with being responsible.

To understand mediamacro you have to recognise that its origins are, in part, the academic consensus that was dominant before the GFC. Governments have two ways they can attempt to manage the aggregate economy: by changing fiscal policy (tax and spend) and by changing interest rates. There are other means (some often called unconventional monetary policy), but none are as reliable and therefore as effective as these two methods. The academic consensus that preceded the GFC was that interest rate changes, delegated to an independent central bank with an inflation target, was a better way to manage the economy than the government changing fiscal policy.

So in this pre-GFC consensus view what should govern fiscal policy at the aggregate level? How big should government deficits be? The pre-GFC academic consensus said that over the long term government debt should be sustainable, which is a jargon word for the ratio of government debt to GDP being stable in the long run, rather than either steadily rising or falling. Of course government debt to GDP could be stable at high or low levels, but academic theory had no strong message on what the optimal level of this ratio should be. In the UK the 1997 Labour government devised fiscal rules to ensure this goal of long run stability was met.

From an academic point of view was there an equivalence in importance between the goals of interest rate policy and fiscal policy? Absolutely not. Academic macroeconomists wrote volumes about what interest rates should be and how central banks should make decisions, because macroeconomic stability was very important. In contrast, debt sustainability was nice to have but, except in rare cases where political failure led to uncontrolled large scale fiscal profligacy, failure to achieve it was no big deal as it could be subsequently rectified. After all, between the 1970s and the 2000s government debt to GDP had almost doubled in the OECD, but economists had no strong evidence that this had had any serious impact on macroeconomic performance. One prominent idea, that higher debt to GDP would raise real interest rates (interest rates less expected inflation), turned out to be a false alarm as global real interest rates fell over this period.

The very long run need for debt stability left journalists with a problem. How were they meant to talk about fiscal policy at the aggregate level if the only test of its appropriateness was some long term goal of sustainability which wasn’t that important anyway? The collective solution they devised was to turn a long term goal into a short term goal, and to overemphasize its importance by morphing sustainability into responsibility. This was so attractive because it made aggregate fiscal policy easily understandable for non-economists: the government became like a household. If its borrowing was too much, journalists could write articles about how taxes would have to rise if the government was to remain fiscally responsible, and if its borrowing fell they could write articles about tax cuts to come. Mediamacro was born, and it was very easy to write and understand.

As long as the pre-GFC academic consensus held, mediamacro was irritating but not wildly wrong. Of course no government is like a household (it is longer-lived, it can create money, and it large relative to the economy), but as long as central banks were doing the stabilisation job this analogy wasn’t doing serious harm. Journalists, it is important to remember, have a difficult job to do in explaining macroeconomics to non-economists.

The academic consensus was shattered by the GFC, although many macroeconomists had seen the writing on the wall well before this by looking at what had happened to Japan. As I have already noted, the global level of real interest rates seemed to be on a downward trend, something macroeconomists often call secular stagnation. With inflation targets at 2%, a real interest of 1% would imply central banks setting a nominal interest rate of 3%. However in a recession, inflation would often be below target, and the central bank needed to achieve real interest rates well below normal levels to generate an economic recovery.

This just wasn't possible, because central bankers also thought there was a lower bound to nominal interest rates at around zero. That meant that central bankers could only achieve at best slightly negative real interest rates, which proved totally inadequate to lift Japan out of its 1990s stagnation and to combat the deep recession that followed the GFC. The upshot was that interest rate changes could no longer be effective at fighting recessions.

As a result during the GFC interest rate policy stopped working, so fiscal stimulus was the only reliable policy in town for stopping the recession and generating a recovery. Any first year economics student would tell you that, and state of the art macro concurred. Macroeconomists whose field this was (like myself), and/or who had seen what had happened in Japan, understood this immediately, although it perhaps took a few years from other economists to get the message that the old consensus was dead.

The Prime Minister at the time of the GFC, Gordon Brown, understood this and used fiscal stimulus as a tool to limit the size of the 2009 recession. The Conservative opposition found it politically convenient not to understand, and instead focused on rising government debt as a sign of 'government irresponsibility' and pledged to introduce tough fiscal contraction (austerity) instead. There were now two different, and competing, stories about what fiscal policy should be doing: the old and much exaggerated story about long run sustainability, and the more relevant story about using fiscal policy to get out of recession. In academic terms the first was downright dangerous during a recovery from recession, while the second was correct.

I invented the term mediamacro because almost all journalists during the austerity period decided to stick with the old story. Mediamacro was now the opposite of the truth, and a deeply damaging message for the public to hear. I tried very hard, along with other more famous macroeconomic bloggers located mainly in the US, to both educate journalists about this error and work out why it persisted.

Unfortunately we faced an uphill struggle for three related reasons. The first was that some well known macroeconomists backed austerity, at least initially. It was clear to me from surveys and other evidence that they were in a clear minority, both in the UK and US, but from 2010 they were in tune with the political consensus so they got a lot of publicity. In the early stages we spent much time successfully debunking their ideas, such that by 2013 Paul Krugman could convincing argue that the intellectual case for austerity had crumbled.

The second reason was that proponents of austerity claimed that without it chaos would occur because the markets would stop buying government debt. Our attempts to explain why this was highly unlikely were unpersuasive after the shock of the GFC. A better approach was to explain why, even if it did happen, it didn’t matter because the central bank would buy the debt under its Quantitative Easing Programme, a point I made in one of my first blog posts.

The third reason this was an uphill struggle was the Eurozone Crisis, where particular EZ governments were having problems selling their debt. To many, including those who should have known better in the IMF, this seemed to validate the austerity narrative. In reality it didn’t, because the European Central Bank did not at the time have a Quantitative Easing programme, and was not providing unlimited support to member countries. The moment the ECB changed its policy in 2012 to do this, the Eurozone Crisis came to an end. (For more detail, see here or here.)

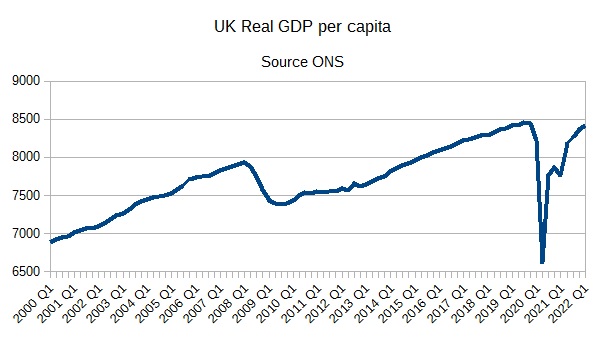

The damage done by austerity, backed up by mediamacro, was huge in economic and political terms, and the mistake was not repeated during the Covid pandemic. Yet mediamacro lives on. Governments still have deficit targets that are too short term, and journalists still write up monthly (!) deficit outturns in terms of their implications for future taxes. Only policy makers in the US understood the need for a fiscal stimulus during the recovery from the pandemic, and as a result major European countries look like they will permanently lose percentages of GDP compared to the US, while still suffering from high inflation.

There are now some very good economic journalists in the media. But how do other journalists move beyond mediamacro, without having to explain everything I have written in this post so far? I think above all else they need to do two things. The first is to understand that the old academic consensus is dead. In simple terms the new academic consensus is that interest rates are still the favoured instrument to deal with inflation (as we are currently seeing), but it is fiscal policy that is the main weapon needed to fight recessions. As a result, if there is a risk of recession or during the recovery phase from recession, deficit targets reflecting debt sustainability go out of the window, and macroeconomic recovery becomes the only sensible goal of a government’s fiscal policy.

The second thing journalists need to do is to stop treating increases in government debt as bad, and falls in government debt as good. It’s just terrible macroeconomics, and will mislead your audience. Is it always bad if a government buys a financial or physical asset by issuing debt? Of course not. Is it bad that government debt rises in recessions? Quite the contrary: if it didn’t because the government stopped it happening the recession would be far worse. Is the high level of most government’s debt today a problem? Not obviously given how low long term interest rates remain. As there is no academic consensus about what the optimal level of government debt is, it would be just wrong for journalists to imply government debt is 'too high'.

Of course what I’m suggesting is not necessarily how policymakers talk about the world. It is also the case that a large part of the print media will persist with mediamacro because it serves a certain ideological perspective. However knowing what the academic consensus is can only improve the quality of impartial economic and political journalism. Good journalists should never just follow a political consensus when it goes against expert opinion without at least recognising what experts are saying. Ignoring knowledge is not being impartial. The austerity period represented, among other things, a major failure of mainstream journalism in the UK and elsewhere.

When there is a consensus among economists does that consensus deserve to be acknowledged? I think among some political journalists there is a cynical view about economics in general, and academic economists in particular. Do they deserve to be called experts when they are always disagreeing with each other and failed to predict the financial crisis (and so on). It would take another post to fully debunk that view. But all I need to say here is that on the two major economic policy issues in the UK over the last 12 years, first austerity and then Brexit, it is the consensus among academic economists that has been proved right, and those that dismissed this consensus as ‘out of touch with the markets’ or ‘project fear’ respectively that have been proved very wrong.